Table of Content

If the property is adjacent to a non residential property the minimum is 10 feet still. Cash out is allowed up to 80% of the value of the home, and a 30 year term is allowed. As a lender I always try to set up the possibility to everyone involved in the transaction of this needing to be done in order to sell or buy a manufactured home. If a borrower is using FHA financing it will always be needed.

Installed on a permanent foundation built according to FHA guidelines. All persons applying must live in the home with the exception of vacation homes. We also have "Live Help" operators standing by 24/7, helping both existing and new customers get the answers to the questions they may have, all in real time. To apply for a loan or to open a new account, select the Open and Apply option once logged in. So, you want to know about any issue that may decrease its value before applying for the loan.

A Few Important in house Manufactured Home Guidelines:

If you are in the market for a used mobile home, your knowledge of this information could make or break your mobile home financing application. A mobile home, also known as modular or manufactured homes, is constructed wholly or in prefabricated portions in a factory. Credit scores as low as 500 can be accepted with atleast 20% down payment. The down payment can be in form of cash, mobile home trade, land equity or a combination of all. Thank you for choosing Mobile Home Spot, the dealer that will help you find your Florida Forever Home! The professionals at Mobile Home Spot are pleased to announce that our buyers needing financial assistance are welcome to work with both CenterState Bank and Central Bank.

This make VA financing the most flexible when it comes to financing manufactured homes. Florida home sales normally take 2-3 weeks, depending on if an appraisal is required. Your Florida loan officer will provide you with a list of items, called stipulations, that we will need you to fax or email to us. Once we have these items and your appraisal/inspection has been completed and cleared, we will be ready to close your Florida mobile home financing loan. An inspection is always required on every Florida mobile home financing loan.

New and Used Mobile Home Loans

When you purchase a manufactured home an engineer is required to come out and inspect the home and make sure that it is up to code. The only way around this is via conventional financing on a home with no additions or changes to the roofline or added decking. We’re well versed in the financing options currently available to buyers of manufactured and modular homes. These include FHA, VA, Land-in-Lieu, and Construction loans. We can help you select the one that best suits your unique situation and needs.

Like conventional financing all mobile home loans are subject to the property qualifying and the buyer financially qualifying. Traditional lenders such as banks, mortgage companies, and credit unions are generally not sources for the required financing to purchase a manufactured home. The majority of our Florida customers live in mobile home parks and/ormanufactured home communities, where the land is leased or rented. We also may be able to provide Florida manufactured or mobile home finance loans if the home sits on a relatives land, and once again is considered personal property.

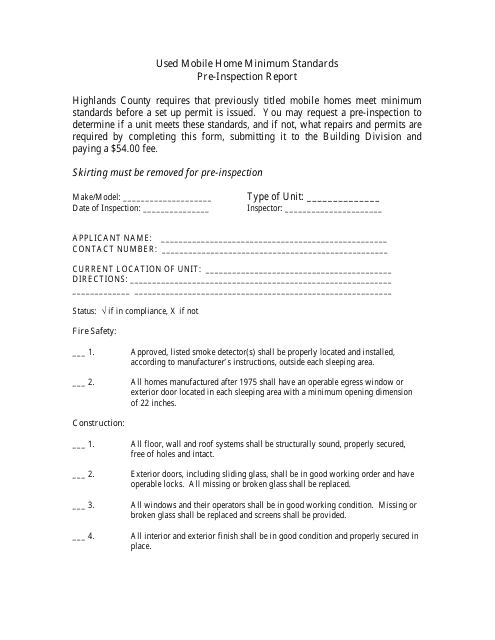

How important is the certification label or HUD Plate?

If you have not registered with us before you will need to create an account to fill out an application. Once you have completed your application, a mortgage loan originator will contact you with a decision on your application. Private Mortgage Insurance-Mortgage insurance is not required on any 21st Mortgage loan. Debt-to-Income Ratiois calculated by dividing your total debts by your income. If this ratio is greater than 43%, you may still be eligible for a loan but additional documentation may be required.

This could not be accomplished by adding thousands of dollars to your new FL mortgage to pay commissions to a mortgage broker. In some cases we can finance single wide manufactured homes. You must have good credit and the loan amount can’t be too small (approximately $150,000 or more). First thing is first, technically a mobile home is a factory built home that was constructed prior to June 15, 1976. Even so people still today call newer manufactured homes mobile homes. The terms people use can change depending where you live but in Florida people often use the term mobile home for manufactured homes constructed after 1976.

FHA and USDA loans also charge a small monthly insurance premium as well to cover the cost of insuring the loan. Florida Modular Homes and the lenders we have teamed up with offer financing for both mobile and modular homes. For both home only financing with no land involved in the transaction and land / home financing where the land purchase or payoff is financed in the same payment as the home.

The HUD regulatory manufacturing standard ensures that American mobile homes are built to last decades if properly maintained. Florida Modular Homes has access to a unique financing program designed for homebuyers who have experienced challenges with their credit. Below we have outlined our basic FL requirements and guidelines to better assist you. Bank Repossessions/HUD Foreclosures– We do not provide financing for foreclosed or repossessed properties that are being purchased from another lender, including HUD.

The Florida mobile or manufactured home must have been previously titled and cannot be a brand new home being sold by a Florida Dealer. When searching and researching mobile homes in Florida it's essential to connect with a knowledgable resource. MH Loans aims to be this resource for first time buyers or those looking for a great refinancing option for thier current mobile home loans. The fastest way to begin the process is to visit the online application or just reach out and call MH Loans today. The manufacturedor mobile homes that we can finance in FL are considered personal property, not real property and/or real estate.

The veteran is now allowed to pay for these items when they couldn’t in the past. We do not require an engineer to inspect the property like FHA or conventional financing to make sure that the manufactured home meets the current HUD guidelines. Additionally the veterans administration will allow a veteran to purchase a manufactured home if it has been moved, but only moved one time.

An appraisal is required if we do not have the value using the above method. Appraisals take into account recent sales from the same community, and surrounding area to determine the market value. Veterans can use their VA entitlement to purchase a manufactured home with no money down! Keep in mind that when purchasing any home that has a well the VA requires both a bacteria water test and a lead water test.

Manufactured home and mobile home loan underwriting process is the same as traditional real estate loans used to purchase single family homes. The underwriting process normally takes six to seven weeks which is comparable to conventional real estate. Loan closing is part of the property closing and usually takes place at a title company or law office local to the area that the property is being purchased. Arrangements can be made to close at alternative locations using a mobile notary/closing agent.

If you can't find that red tag, it will be impossible to find many mortgage lenders to finance a loan. See our Communication Terms and Conditions, which includes opt-out instructions. The property and home information presented is believed to be accurate at the time of posting; however, there may be some inaccurate or out of date material listed. The information listed, including make, model, size, year of manufacture, availability, floor plan, features, acreage, price and other information, are all subject to change without notice. Floor plan dimensions and square footage are approximate and based on length and width measurements from exterior wall to exterior wall. VA insured loans are a benefit for qualified Veterans of the United States Armed Services allowing them to purchase a Factory Built Home for as little as $500 down with no monthly mortgage insurance premiums.

No comments:

Post a Comment